- 4 Unexpected Things I’ve Learned From Buying My First Mobile Home Park

- How Ironic: America’s Rent-Controlled Cities Are Its Least Affordable

- U.S. homes are still a bargain on the international market

- Getting The Best Possible Quality Photos On MLSs and Syndicated Sites

- Home buyers in these markets have the upper hand

How to Use Cost Segregation to Increase Depreciation

When purchasing a property, the vast majority of landlords simply depreciate the improvement portion of the property over a 27.5 year (residential) or 39 year (commercial) period. If you read my prior article, you’ll know how to determine the improvement value of the property you purchased to maximize your annual depreciation. But what if I told you we can take that one step further and substantially increase your allotted depreciation in the first couple of years you own the property?

Depreciation is great because it’s a phantom expense; however, the major downside is that it’s a slow method of cost recovery. As a CPA, my goal is to maximize the amount of money my clients keep in their pockets, and a great way to achieve that goal is to frontload depreciation via cost segregation.

What is a Cost Segregation Study?

A cost segregation study allows landlords to take larger deductions by means of frontloading depreciation in the early years of a property’s life. The study will identify assets that are separate from the building structure (e.g. personal property and land improvements), classify those items within the General Depreciation System (GDS) and assign the items a “life” or number of years to depreciate the asset.

If you know anything about cost segregation studies, you’ll know that they are expensive. Current market rates are anywhere between $10,000 to $20,000. This is mainly due to the complexity of the study and the cost of the professionals (usually engineers) performing the study. However, you can perform a cost segregation study yourself or with your CPA and focus on the items for which you can determine a fair market value.

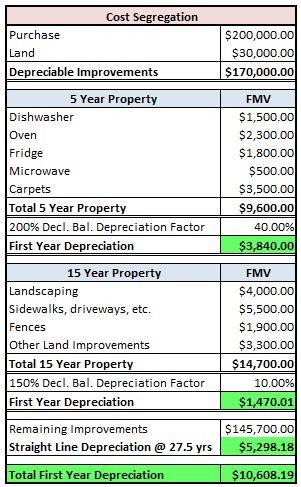

Let’s look at an example of how cost segregation can help your rental real estate business. The first table below depicts a standard scenario in which the purchase price is only divided between the land and improvements, which are subsequently depreciated over 27.5 years. The next table assumes that a cost segregation study of some degree is performed, and as a result, the landlord is able to take $4,426 more in depreciation during the first year of the asset’s life. Of course these are made up numbers, but you can catch my drift.

Frontloading Your Depreciation

When you break out assets, such as personal property and land improvements, into GDS classes, you apply a shorter life to those assets and get to utilize an accelerated depreciation method, which will benefit you more in the short-term. This is what I was referring to as “frontloading” your depreciation deduction.

GDS five year property, such as appliances and carpet, will be depreciated using the 200% declining balance method. Using the straight line method, one would depreciate a five year property 20% each year, but using the 200% declining method, you accelerate your depreciation by multiplying the straight line percentage by a factor of two. So really, we get to depreciate the value by 40% each year. The catch is that you have to apply the 40% to the book value of the asset (the cost minus accumulated depreciation), so in future years, your depreciation write-off will decrease.

For example: You have a five year asset worth $10,000. In the first year, you depreciate it $4,000 ($10,000 x 0.40). In the second year, your depreciation shrinks to $2,400 [($10,000 – $4,000) x .4]. As you can see, the closer you get to the end of the useful life, the less your yearly depreciation write-off will become.

GDS 15 year property uses the 150% declining balance. The same logic from above is applied, but instead of using a factor of 2, you will use a factor of 1.5. Frontloading your depreciation can be a critical tax planning strategy to utilize because as we all know, a dollar today is worth more than a dollar tomorrow.

Focus on Items Where a Fair Market Value is Easily Identified

Leave the crazy stuff to the engineers. Instead, focus on the assets where a fair market value can be easily and readily determined, such as personal property and land improvements. If the asset is almost new, you can research the cost to replace the asset and use that cost as the asset’s tax basis. However, if the asset is a bit older, you will need to determine the current salvage value, or in other words, the amount you would be able to sell the asset for in today’s market. This is when it is a good idea to get with a CPA ,as there are a number of ways of determining the asset’s salvage value.

In addition to calculating the salvage value, you will want to substantiate your estimate with factual data from the actual sales. You can check Craiglist ads and eBay ads, preferably those that have been closed due to sales. You can call up or send surveys to vendors who trade those items and even ask them to provide you with a hard quote of what they would buy your asset for. If you have an expensive asset, you may wish to have a professional appraisal performed.

Most importantly, when determining a value, keep detailed documents defining your methodology and showing support for your calculations. Your documents should be detailed enough that a third party knowing nothing about you can come in and 100% understand and agree with your study.

Does a Cost Segregation Study Increase Audit Risk?

Get ready for a classic answer: it depends. It’s difficult to determine the factors that trigger an audit, and a cost segregation study alone will not substantially increase your audit susceptibility. However, if you are performing a cost segregation study for a property placed in service during a prior year (commonly known as a look-back analysis), you will need to file Form 3115, which may be reviewed by an IRS committee and can inherently increase your audit risk.

If you document your findings expecting to one day be audited, you will be fine. It’s important to note that the IRS has not established any requirements or standards for the preparation of cost segregation studies. While the tax courts have previously addressed component depreciation, they have not specifically addressed the methodologies of cost segregation studies. Despite the lack of specific requirements, you will still need to substantiate your depreciation deductions and classifications of assets. In the event of an audit where estimates are used to determine fair value, the methodology and the source of any cost data should be clearly documented.

I’ll wrap up with the elements of a “quality” cost segregation study and report as defined by the IRS. If you follow their guidelines, you are more likely to be protected in the event of an audit. You may read more about them here.

A quality cost segregation study will have the following elements:

- Preparation by an Individual With Expertise and Experience

- Detailed Description of the Methodology

- Use of Appropriate Documentation

- Interviews Conducted With Appropriate Parties

- Use of a Common Nomenclature

- Use of a Standard Numbering System

- Explanation of the Legal Analysis

- Determination of Unit Costs and Engineering “Take-Offs”

- Organization of Assets into Lists or Groups

- Reconciliation of Total Allocated Costs to Total Actual Costs

- Explanation of the Treatment of Indirect Costs

- Identification and Listing of Section 1245 Property

- Consideration of Related Aspects (e.g., IRC § 263A, Change in Accounting Method and Sampling Techniques)

A quality cost segregation report will have the following elements:

- Summary Letter/Executive Summary

- Narrative Report

- Schedule of Assets

- Schedule of Direct and Indirect Costs

- Schedule of Property Units and Costs

- Engineering Procedures

- Statement of Assumptions and Limiting Conditions

- Certificate

- Exhibits

100% Secure

100% Secure

You must be logged in to post a comment Login